Central Limit Theorem

Introduction

Learning objectives of this asynchronous lesson:

- Recognize that estimates derived from samples may not precisely

reflect the true population parameter

- Understand how to apply the Central Limit Theorem to characterize the uncertainty from a sample based estimate

- Calculate the 95% confidence interval for a sample average using Normal approximation

Dataset

For this set of examples, I will use the Cyberville families data. Recall that this is a population dataset. In order to calculate sample statistics, we will take a simple random sample of 400 observations.

data <- read.csv(url("https://laurencipriano.github.io/IveyBusinessStatistics/Datasets/families.csv"),

header = TRUE)

## suppress scientific notation for ease of reading numbers

options(scipen=99) Population statistics

Usually we can’t know the population statistics. But, because this dataset is a complete census of the Cyberville city, we can calculate the population average and population standard deviation.

We can use these measures to compare to the results we obtain from our sampling studies.

# Calculate the true population mean of Income

true.avg <- mean(data$INCOME)

# Calculate the true population standard deviation of Income

true.sd <- sd(data$INCOME)

print(cbind(true.avg, true.sd))> true.avg true.sd

> [1,] 41335.51 32037.62Population distribution

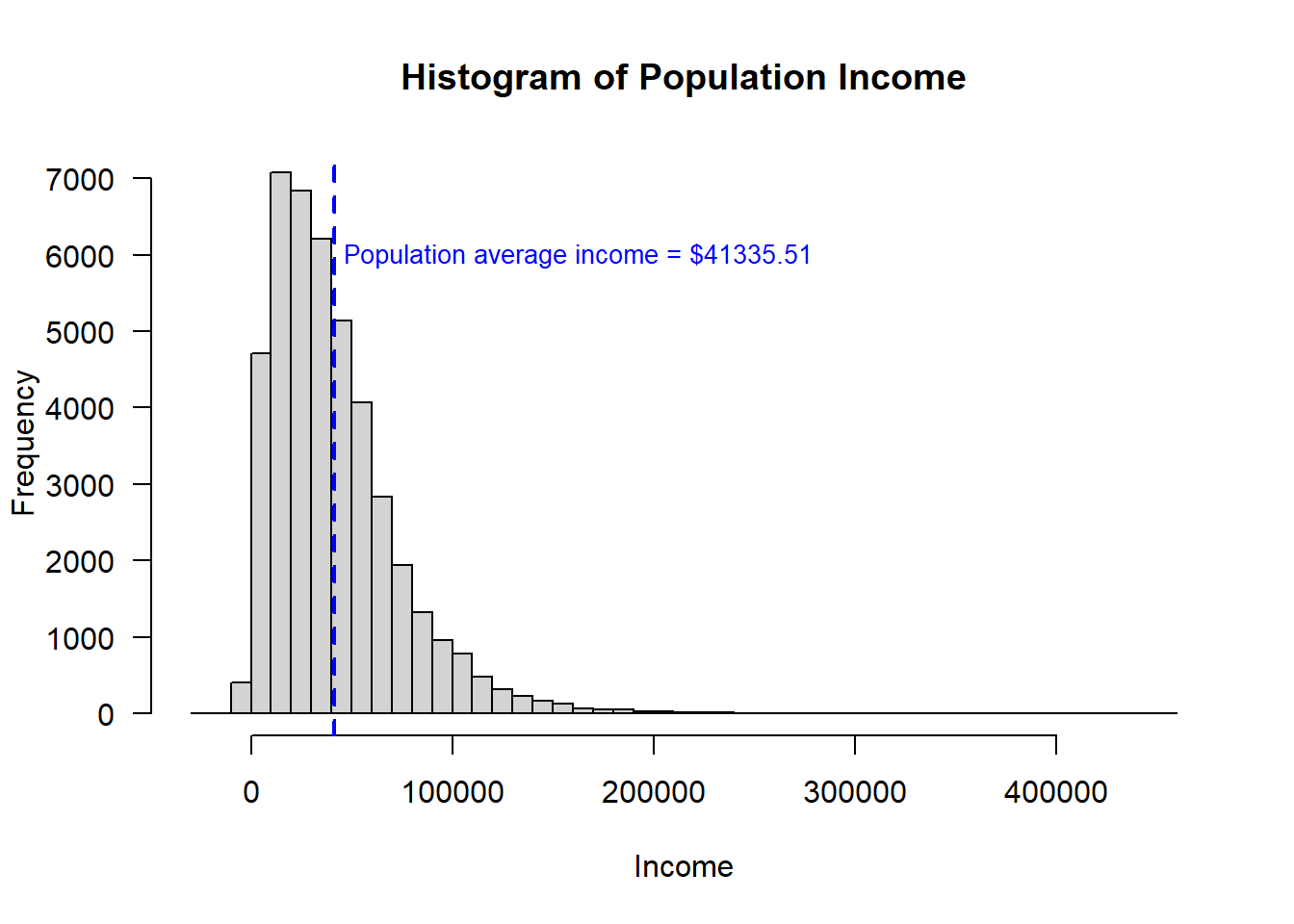

Note, that the actual population distribution of income is not normally distributed. It is right or positively skewed.

# Histogram of population income

hist(data$INCOME,

breaks = 40,

xlab = "Income",

main = "Histogram of Population Income",

las = 1 ) # orients the y-axis labels to read horizontally

abline(v=true.avg, # draw a line at the population mean

col = "blue",

lwd = 2, # lwd is the line width

lty = 2) # lty is dashed

text(x = true.avg + 5000,

y = 6000,

adj = 0, # positions the text box to the left of the coordinates

labels = paste0("Population average income = $", format(true.avg, nsmall = 2)),

col = "blue",

cex = 0.85) # cex is font size

Performing a study

If a researcher wanted to know about the population about Cyberville, performing a census would be expensive and and inefficient. It is also possible that it would be very difficult to actually achieve a complete census and the people who are most difficult to collect information from may have similar features For example, it is very difficult to capture homeless individuals in population census. If the census systematically misses a segment of the population, the census estimates will not represent true population statistics.

When conducting a sample, researchers spend time and effort sampling hard-to-reach demographics to ensure that they are correctly represented in the sample. When that is done, a sample average can be more accurate that a costly census estimate of the average.

However, a sample estimate will have uncertainty. One of the benefits of probability-based sampling methods is that the uncertainty can be characterized and quantified.

Probability-based sampling methods include

- (simple) random sampling

- systematic sampling

- stratified random sampling

- cluster sampling

Many large population based studies and political polls use stratified random sampling. Challenges to stratified random sampling are discussed in several good articles about political polling in the 2016 US Election:

- What Pollsters have changed since 2016 - and what still worries them about 2020

- What the Polls say about Harris that the Trump team doesn’t like

For today’s lesson, we will implement the simplest of these methods simple random sampling.

Generate a sample

We will randomly sample 400 people for our study estimating average income.

n <- 400 # sample size

select.obs <- sample(1:nrow(data), n) # from a list of numbers (1, 2, 3, ... ), select n of them at random

# from the original data frame, name a new dataset only keeping the observations in the sample

study.data <- data[select.obs, ] Calculating sample statistics

With the sample data, we can calculate the average and standard deviation of the sample.

# Calculate the sample mean of Income

sample.avg <- mean(study.data$INCOME)

sample.avg> [1] 38881.47# Calculate the sample sd of Income

sample.sd <- sd(study.data$INCOME)

sample.sd> [1] 33659.31If you run the last two sections of code repeatedly, you will find that each time a new sample is selected the sample mean is a different number.

Of course, as a researcher, you would only ever see the one sample you actually get. But, we can explore the randomness of sampling by running a simulation in which we can repeat the study many times by taking different samples from the available population data in this case.

Let’s pretend to be able to do the study in which we randomly sample 400 people 5000 times.

M <- 5000 # number of times we will simulate running the study

n <- 400 # sample size

# initialize an empty vector to store the outcome of the study

sample.reps <- data.frame(avg = rep(NA, length = M), sd = rep(NA, length = M))

# using a loop, run the study many time, recording the average income each time

for (m in c(1:M)){

# from the data frame "data" randomly sample n observations, making a new dataset "study.data"

select.obs <- sample(1:nrow(data), n)

study.data <- data[select.obs, ]

# Calculate the sample mean of Income

sample.reps$avg[m] <- mean(study.data$INCOME)

sample.reps$sd[m] <- sd(study.data$INCOME)

}Distribution of the sample means

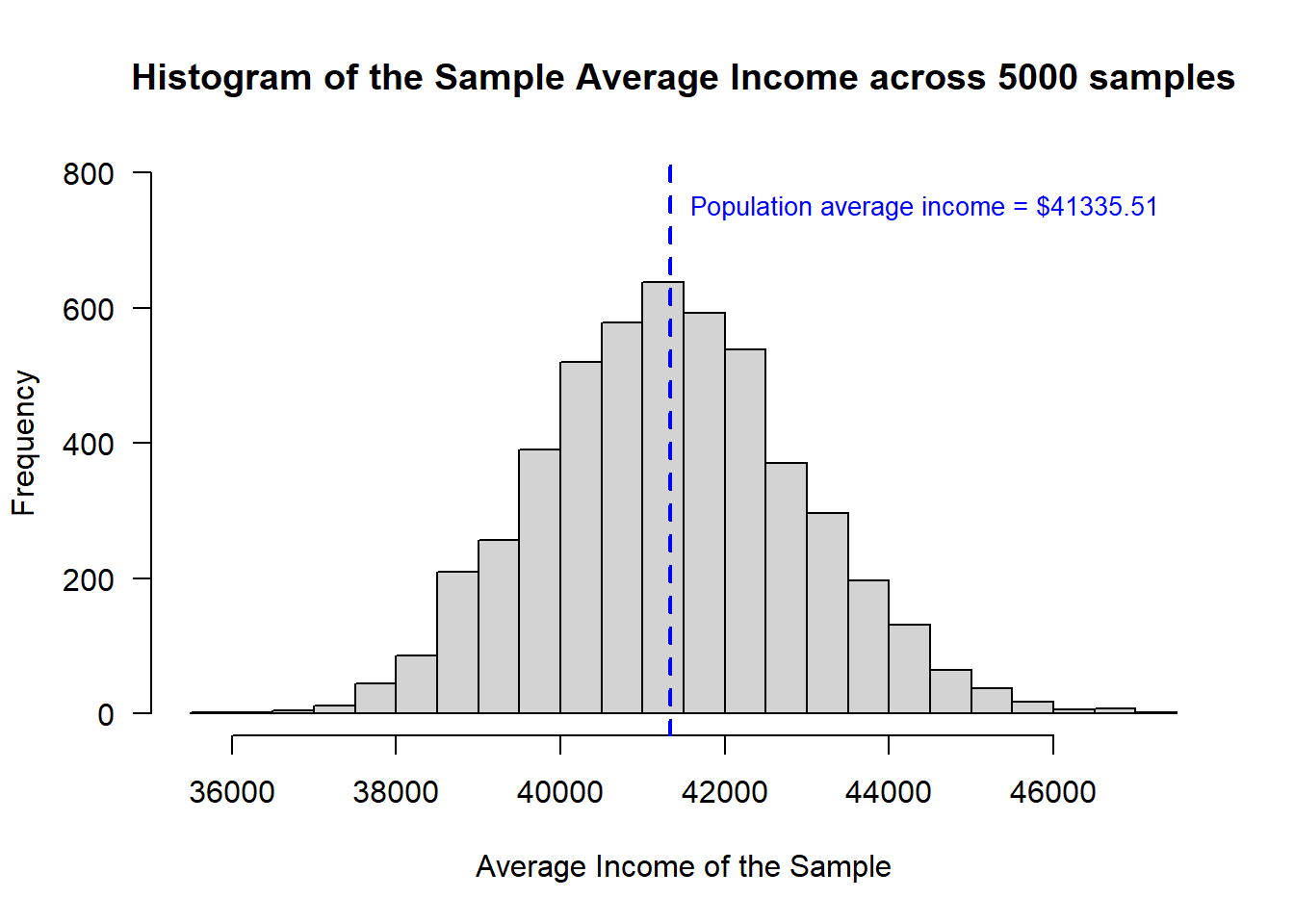

To visualize the distribution of the outcomes from simulating the sampling 1000 times, we can present a histogram of the sample mean and then draw a line where we know the actual population mean is.

# draw a histogram of the sample average income

hist(sample.reps$avg,

breaks = 20,

xlab = "Average Income of the Sample",

main = "Histogram of the Sample Average Income across 5000 samples",

ylim = c(0, 800),

las = 1 ) # orients the y-axis labels to read horizontally

abline(v=true.avg, # draw a line at the population mean

col = "blue",

lwd = 2, # lwd is the line width

lty = 2) # lty is dashed

text(x = true.avg + 250,

y = 750,

adj = 0, # positions the text box to the left of the coordinates

labels = paste0("Population average income = $", format(true.avg, nsmall = 2)),

col = "blue",

cex = 0.85) # cex is font size

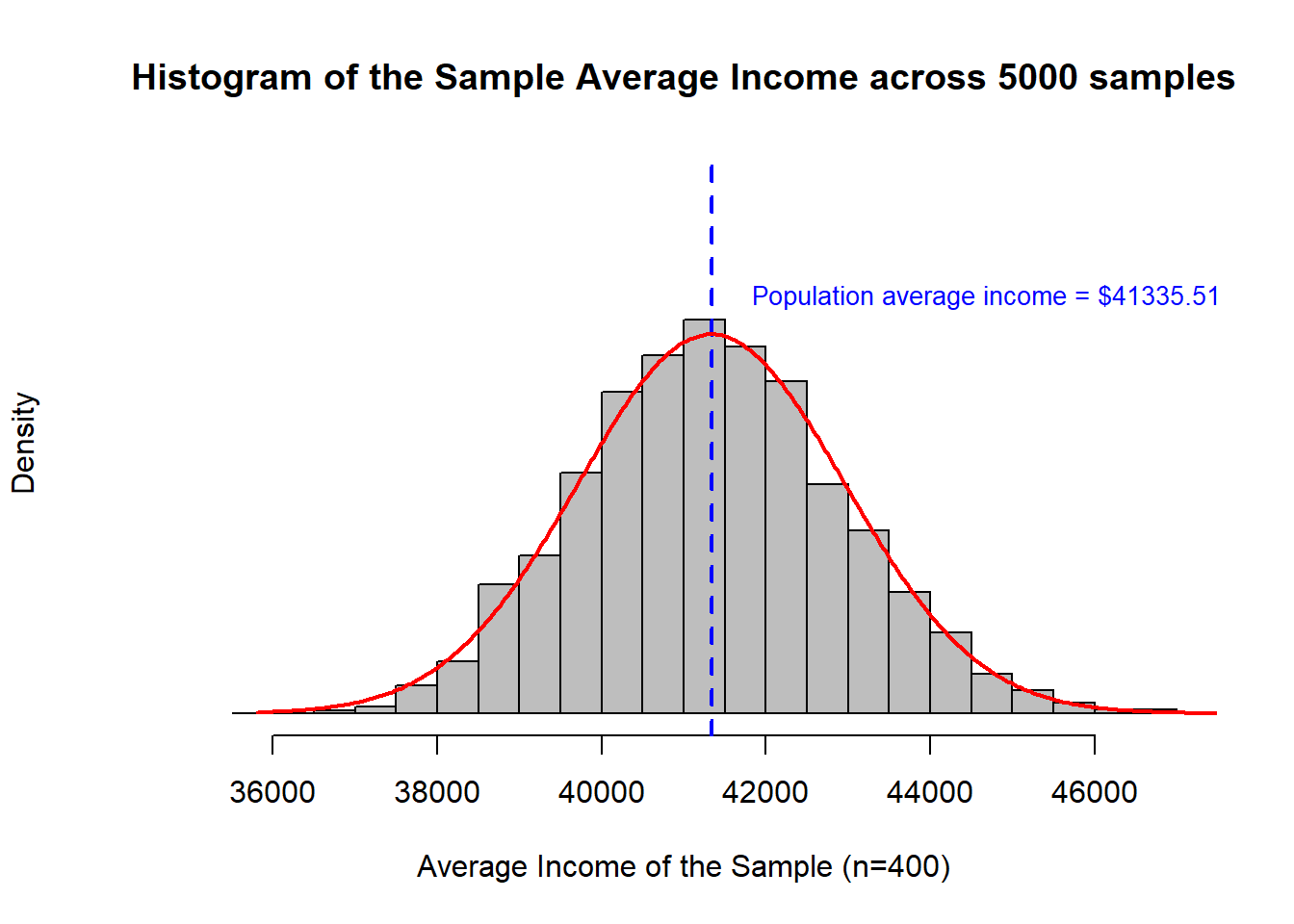

This looks so Normally distributed!! Let’s overlay a Normal distribution on this graph to visualize how well it fits.

So, even though the underlying population distribution was not Normally distributed, the uncertainty in the sample average for income is Normally distributed.

Central Limit Theorem

The Central Limit Theorem is the formal mathematical statement of what you have just observed.

The CLT states that the distribution of uncertainty around the sample mean converges to the Normal distribution where the mean of the distribution is the sample mean and the standard deviation is the standard error.

The standard error is the special name given to the standard deviation representing the sampling uncertainty of an estimate. The calculation of the standard error requires knowing the population standard deviation. It is a special case when you don’t know the population average but you do know the population standard deviation. And, so, it is common to use the sample standard deviation as the best estimate of the population standard deviation.

\[ \text{SE} = \frac{SD}{\sqrt{n}} \]

Because the sample standard deviation is also an uncertain estimate, this increases uncertainty in the mean and changes the Normal distribution to a t distribution. When the sample size is relatively small (< 30 observations), this matters and you should be careful to use the t distribution. Generally, the Normal distribution is appropriate and reasonable to use directly.

The distribution converges to Normal faster when

- the underlying distribution is Normal

- the underlying distribution has smaller (vs. larger) variance

- the underlying distribution doesn’t have “fat tails”

- the underlying distribution is symmetrical (i.e., isn’t too skewed)

- the size of the sample increases

Because of the Central Limit Theorem, estimating 95% confidence intervals around a sample average using the Normal distribution is both common and highly accurate when compared to exact or bootstrapped intervals.

Uncertainty around a sample mean

The Central Limit Theorem tells us that that the uncertainty from sampling is Normally distributed around the sample mean where the standard deviation is the standard error.

Now, relying on the Normal distribution, we can calculate the 95% confidence interval for that first sample of 400.

# Recall our sample data was 'study.data'

# Calculate the sample mean of Income

sample.avg <- mean(study.data$INCOME)

# Calculate the sample sd of Income

sample.sd <- sd(study.data$INCOME)

# Calculate the standard error for the study where n = 400

se <- sample.sd / sqrt(n)

# Use the se and the Normal distribution to calculate the 95% CI

lowerCI = sample.avg + qnorm(0.025, mean = 0, sd = 1) * se

upperCI = sample.avg + qnorm(0.975, mean = 0, sd = 1) * se

print(cbind(sample.avg, lowerCI, upperCI))> sample.avg lowerCI upperCI

> [1,] 42300.82 39203.17 45398.48Interpreting confidence intervals

In plain language, there is a 95% chance that the true population mean is within the 95% confidence interval.

Looking back on our 5000 replications of the single study, we can see that this is true.

Specifically, we can identify how many of our 5000 studies were randomly such terrible samples that the 95% confidence interval did not contain the true population mean.

# Recall our dataframe from above holding the sample average and sample standard deviation from the 5000 replications

# We now add columns in which we will calculate the standard error and the lower and upper 95% CI

sample.reps$se <- sample.reps$sd / sqrt(n)

sample.reps$lowerCI <- sample.reps$avg + qnorm(0.025, mean = 0, sd = 1) * sample.reps$se

sample.reps$upperCI <- sample.reps$avg + qnorm(0.975, mean = 0, sd = 1) * sample.reps$se

# Next we will add a column to report whether the true population mean is *lower* than the lower CI or the true population mean is *higher* than the upper CI

sample.reps$outBounds <- 0 # initialize the column

sample.reps$outBounds[ true.avg < sample.reps$lowerCI ] <- 1

sample.reps$outBounds[ true.avg > sample.reps$upperCI ] <- 1

# what % of study replications reported 95% CI that did not include the true population average?

sum(sample.reps$outBounds)/m> [1] 0.0492I hope it is not too much of a surprise that this is really close to 5%!

Next: Elements of a Statistical Test